Introduction to Insurance

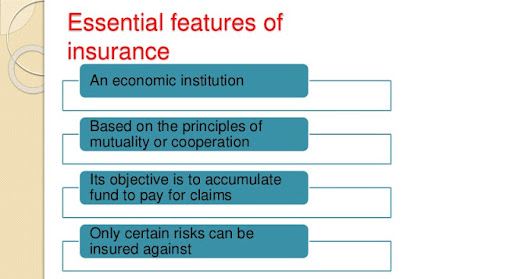

Insurance is a financial arrangement wherein a policyholder pays premiums to an insurer in exchange for coverage against specified risks or losses. It functions as a risk management tool designed to provide financial protection and mitigate uncertainties. By pooling resources from policyholders, insurance companies ensure compensation for covered incidents like accidents, illnesses, property damage, or even death.

The concept of insurance is underpinned by principles such as risk transfer, policyholder participation, and indemnity. Insurance agreements are formalized through contracts detailing coverage terms, premium amounts, and claim procedures. This mechanism promotes economic stability and fosters both individual and business resilience against unforeseen adversities.

Definition of Insurance

Insurance is a contractual agreement between an individual or entity (the insured) and an insurance provider (the insurer) designed to mitigate financial risk. In exchange for periodic payments, known as premiums, the insurer promises to compensate the insured for specific losses, damages, or liabilities that may occur, as outlined in the policy.

This mechanism functions based on the principle of risk pooling, where multiple parties contribute to a shared fund to protect against uncertain events. The scope of coverage, exclusions, and terms are detailed in the insurance policy, ensuring clarity and legal backing for both parties involved.

How Insurance Works

Insurance operates as a risk management tool, allowing individuals or entities to transfer the financial burden of potential losses to an insurer. Policyholders pay premiums to the insurance company in exchange for coverage. The process begins with an assessment of risks, followed by issuing a policy that outlines terms, coverage limits, and exclusions.

When a covered event occurs, the insured files a claim. The insurer evaluates the claim to determine its validity based on the policy terms. Upon approval, compensation is provided to mitigate the financial impact. This system ensures shared responsibility and financial protection across a broad pool of contributors.

Types of Insurance: Life Insurance

Life insurance is a contract between an individual (policyholder) and an insurer, in which the insurer guarantees a designated beneficiary a financial benefit upon the policyholder’s death. It serves as financial protection, covering expenses such as funeral costs, outstanding debts, or income replacement for dependents.

Main Types of Life Insurance:

- Term Life Insurance: Provides coverage for a specific period, typically 10, 20, or 30 years, with lower premiums.

- Whole Life Insurance: Offers lifetime coverage and includes a cash value component that grows over time.

- Universal Life Insurance: Features flexible premiums, adjustable coverage, and a savings component.

Life insurance policies generally require regular premium payments and may include optional riders for added benefits, such as critical illness coverage.

Types of Insurance: Health Insurance

Health insurance is designed to cover medical expenses and provide financial protection against the high costs of healthcare services. It typically includes coverage for medical, surgical, and prescription drug expenses, as well as preventive care. Policies vary, offering plans with diverse benefits to suit individual and family needs.

Common Features of Health Insurance Plans:

- Premiums: Regular payments required to keep the policy active.

- Deductibles: The amount the insured must pay out-of-pocket before coverage begins.

- Co-payments/Coinsurance: Shared costs between the insured and the insurer for specific services.

- Network Providers: Healthcare professionals and facilities covered under the plan.

Health insurance may be obtained through employers, private insurers, or government programs like Medicaid and Medicare.

Types of Insurance: Auto Insurance

Auto insurance safeguards against financial losses caused by accidents, theft, or damage to vehicles. It typically encompasses several coverage types designed to address various situations. Common coverage options include:

- Liability Coverage: Pays for damages or injuries to others if the policyholder is at fault.

- Collision Coverage: Covers repairs to the policyholder’s vehicle after a collision, regardless of fault.

- Comprehensive Coverage: Protects against non-collision events such as theft, vandalism, or natural disasters.

- Uninsured/Underinsured Motorist Coverage: Provides protection if the other driver lacks adequate insurance.

Premium rates depend on factors like vehicle type, driving history, and location. Auto insurance is often legally required, ensuring financial protection for all road users.

Types of Insurance: Home Insurance

Home insurance, also known as homeowners insurance, provides financial protection against damage or loss related to one’s property. It typically covers the physical structure of the home, personal belongings inside the property, and liability for accidents that occur on the premises. Policies can vary but often include the following key coverages:

- Dwelling Coverage: Covers damage to the physical structure due to risks like fire, hail, or storms.

- Personal Property Coverage: Protects against loss or theft of belongings.

- Liability Protection: Offers coverage for legal expenses if someone is injured on the property.

Optional add-ons, such as flood or earthquake insurance, provide additional safeguards depending on location-specific risks.

Types of Insurance: Business Insurance

Business insurance protects organizations against potential financial losses arising from unexpected events. It includes various coverages tailored to meet specific business needs. Common types include:

- General Liability Insurance: Covers claims related to bodily injuries, property damage, or advertising injuries caused by business operations.

- Property Insurance: Protects physical assets such as buildings, equipment, and inventory from losses due to disasters like fire or theft.

- Professional Liability Insurance: Also known as errors and omissions insurance, it safeguards against negligence claims related to professional services.

- Workers’ Compensation Insurance: Provides benefits for employees injured on the job, covering medical expenses and lost wages.

- Business Interruption Insurance: Compensates for income loss during disruptions caused by events like natural disasters.

Businesses should evaluate industry-specific risks before selecting appropriate coverage to ensure comprehensive protection.

Factors to Consider When Choosing Insurance

When selecting an insurance policy, various critical factors must be evaluated to make an informed choice. These factors ensure that the coverage suits individual needs and financial goals:

- Coverage and Benefits: Analyze the scope of coverage and ensure it aligns with potential risks and personal requirements. Consider whether the policy addresses health, property, liability, or other specific needs.

- Premium Costs: Evaluate the affordability of premiums while considering long-term financial commitments. Review how premium variations impact coverage limits and benefits.

- Policy Exclusions: Carefully read the exclusions section to understand what is not covered. This prevents unpleasant surprises during claim settlements.

- Provider Reputation: Assess the credibility and financial stability of the insurer. Research customer reviews, claim settlement ratios, and industry ratings to verify reliability.

- Flexibility and Add-ons: Determine if the policy allows customization through riders or add-ons to enhance coverage. Flexibility ensures adaptability to evolving needs.

- Claim Process: Investigate the efficiency and ease of the claim process, including required documentation, timelines, and customer support effectiveness.

Proper evaluation of these factors helps secure suitable coverage while avoiding unexpected gaps or excessive costs.

Conclusion

Insurance serves as a vital mechanism for managing risks and safeguarding against unforeseen financial losses. By pooling resources, policyholders benefit from shared responsibility and protection in exchange for premiums. Various types of insurance, such as life, health, and property, address distinct needs, ensuring comprehensive coverage across different aspects of life. Key features, including premium payments, policy terms, and exclusions, allow for tailored options based on individual requirements. Understanding these components empowers individuals to make informed decisions while securing financial resilience. As a cornerstone of financial planning, insurance supports long-term security and stability for both individuals and businesses alike.